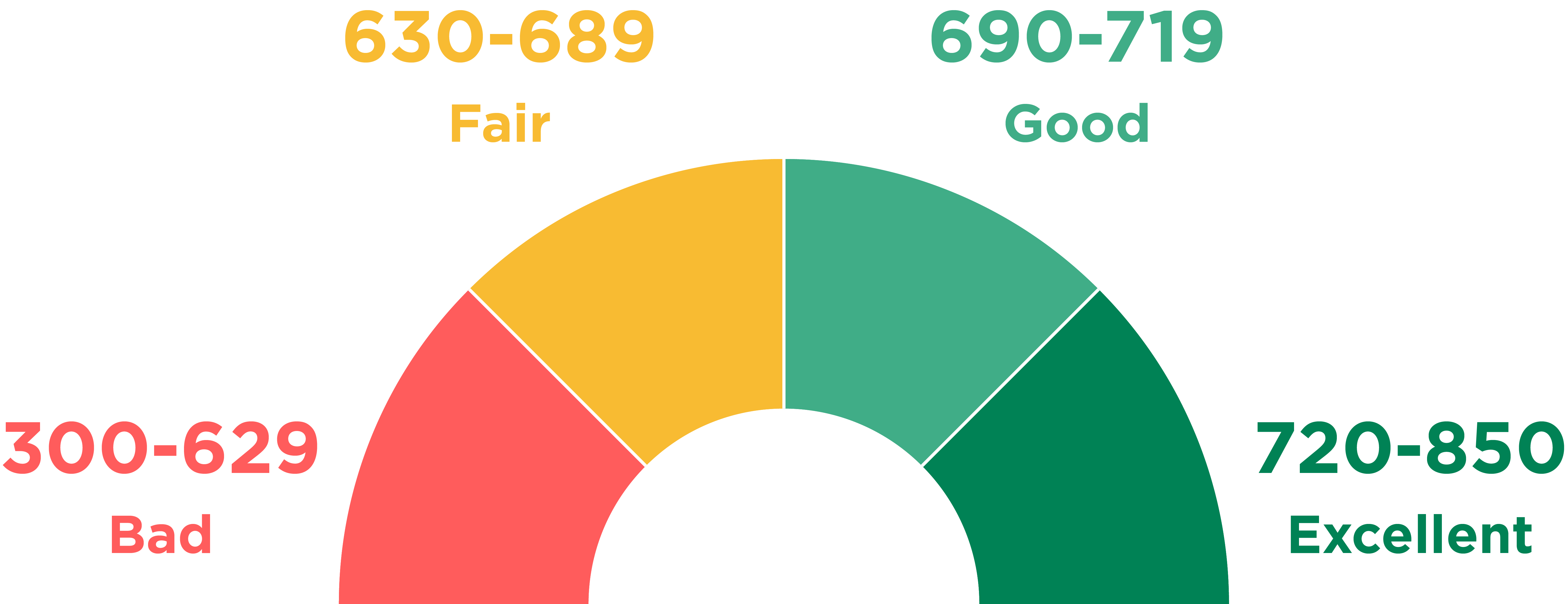

Step one: Pay the bills of yours on time

Step one: Pay the bills of yours on time

The payment history accounts of yours for about thirty five % of your credit score much more than every other component. If perhaps you’ve a reputation of having to pay bills late, you have to begin paying them on time. If you have missed payments, get present and stay current. Each on-time payment updates good information to the credit report of yours. The greater the history of yours of having to pay bills on time, the taller that part of the credit score of yours is going to be.

Step two: Review your credit report

* Errors occur, so review the report of yours carefully for:

* Accounts which are not yours

* Accounts together with the bad account date or perhaps credit limit listed

* Names as well as Social Security numbers which are not yours

* Addresses in which you have never ever lived * Negative info, including late payments, much older than 7 years. (Late payments are only able to legally remain on the credit report of yours for 7 years.)

Under the Fair Credit Reporting Act, the 3 national bureaus – Equifax, Experian, and TransUnion – and the creditors of yours are accountable for fixing mistakes on the report of yours. The Federal Trade Commission (FTC) site has detailed measures for fixing mistakes, in addition to a sample dispute letter. When you find accounts which are not yours and suspect you have been the victim of identity theft, you will have to position a fraud alert on the credit report of yours, near those profiles and file a police report along with a complaint with the FTC.

Step three: Pay down your card balances

The quantity of debt you’ve is heavily scrutinized for the score of yours. Your complete claimed debt owed is taken into consideration, in addition to the number of profiles with great balances and just how much available credit have been used. The total reported debt is when compared to complete credit readily available to figure out the debt-to-credit ratio of yours. The credit score of yours is able to suffer if those numbers are extremely close together. The best plan of yours for lowering the debt of yours is making a scheme paying it all. Although it might look like a smart move, do not consolidate debt onto a single lower interest card. Credit inquiries and opening new credit is able to reduce the credit rating of yours, at minimum in the temporary. Closing classic cards with good credit limits also can throw off the debt-to-credit ratio of yours. In case a brand new credit offer is simply too great to pass up, keep the total quantity of yours of credit offered extremely high by not closing any older credit cards.

Step four: Use Credit

You have to use credit frequently for creditors to update the credit report of yours with current, accurate information. While paying out with money or maybe a debit card might allow it to be a lot easier to hold to a budget, a cash only lifestyle does not much to improve the credit score of yours. The simplest way to utilize credit is by using a charge card, particularly in case you are attempting to boost the score of yours to get an installment loan. If you’ve a well used charge card, start making use of it responsibly once again. A very long credit history is a good determining factory for the credit score of yours, therefore making an inactive account busy once again might be beneficial. Even though you have to create the effort to make use of credit regularly, just charge almost as you are able to pay off. Maintain your credit balances low and so as never to damage the debt-to-credit ratio of yours.

Step five: Monitor the report of yours

Keeping a careful eye on the credit report of yours is going to let you find out if the hard work of yours is paying off. Credit monitoring enables you to monitor account activity. You will be also instantly tipped off about any fraudulent activity. The credit bureaus and also FICO provide credit monitoring services, which usually cost you approximately fifteen dollars per month to monitor all 3 of the credit accounts of yours along with scores. You can additionally use Credit Karma or any other free sites alike.

Step 6: When You are looking for a loan, get it done easily.

This is a hack as a result of the lag time in between the lenders as well as the three bureaus.

If you use for a mortgage, the lender is going to “run the credit” of yours —that is, send out an inquiry to among the credit rating agencies to discover exactly how creditworthy you’re. A lot of such inquiries are able to hurt the FICO score of yours since that can indicate you are attempting to borrow money from a number of sources. Naturally, you are able to generate a great deal of inquiries doing a thing perfectly reasonable— like searching for the most effective auto or mortgage loan by applying to a variety of various lenders. The FICO scoring system is created to permit this by thinking about the length of your time about which many queries are made. Attempt to perform all of your loan shopping in thirty days, therefore the inquiries get batched collectively along with its apparent to FICO that you’re loan shopping